CEO essay

NVIDIA Under Pressure: How Etched and Specialized Chips Are Reshaping AI Infrastructure

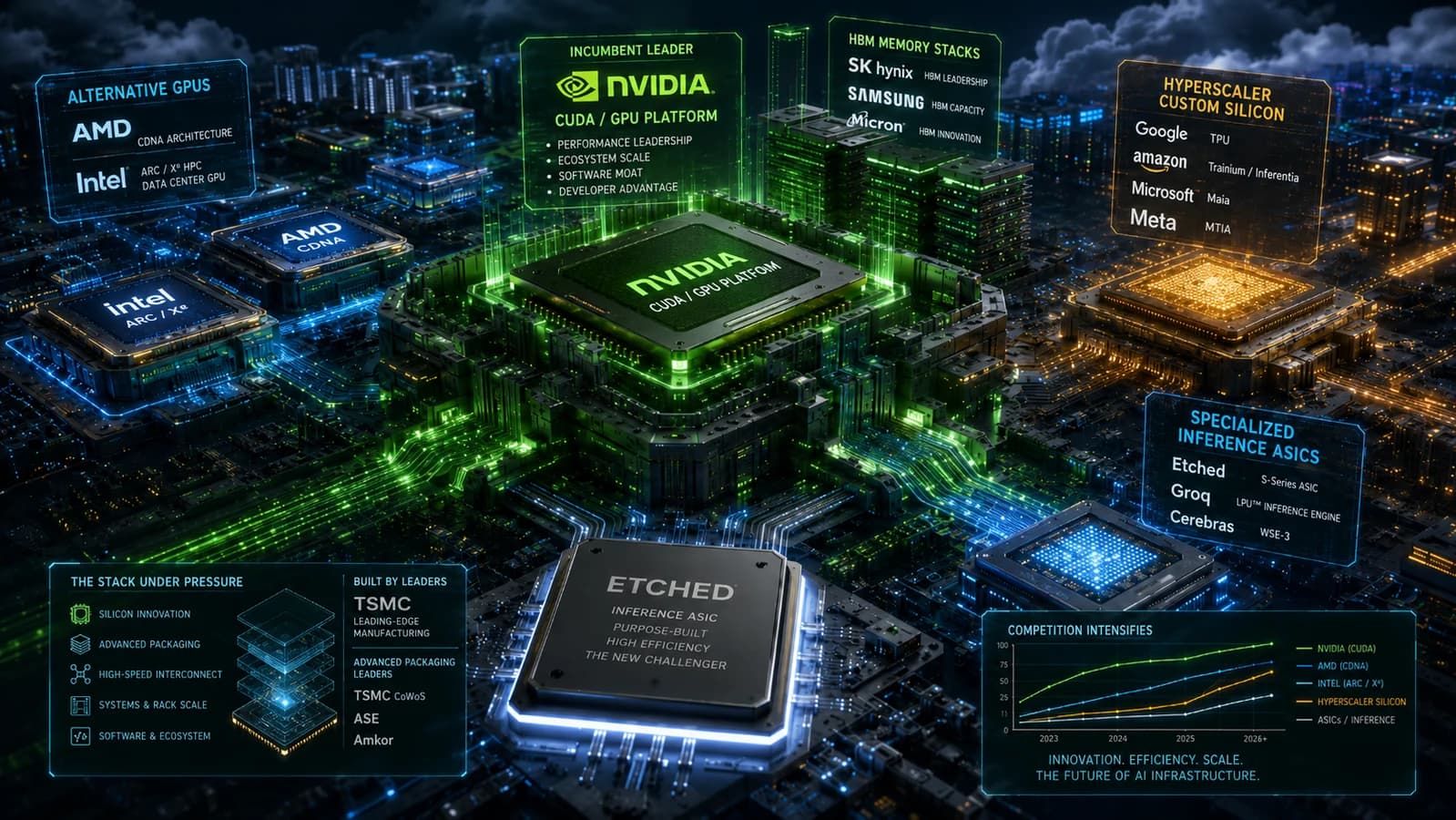

NVIDIA remains the dominant force in artificial intelligence infrastructure. Its strength is not limited to GPUs. It also controls a mature software ecosystem, networking technologies, development tools and years of operational experience i...

Main idea

NVIDIA remains the dominant force in artificial intelligence infrastructure. Its strength is not limited to GPUs. It also controls a mature software ecosystem, networking technologies, development tools and years of operational experience in large-scale AI clusters.

But the market is changing.

NVIDIA is no longer competing only with AMD and Intel. Pressure is also coming from hyperscalers developing custom silicon, specialized ASIC companies, HBM suppliers, advanced packaging providers and software platforms designed to reduce dependence on a single hardware architecture.

The key shift is that customers are moving away from peak-performance comparisons and focusing on real-world economics:

* cost per token; * energy consumption; * hardware utilization; * delivery timelines; * scaling costs; * migration complexity; * dependence on a single supplier.

Etched Is Challenging the Need for General-Purpose GPUs

Etched is one of the most interesting emerging competitors.

The company is not trying to build another general-purpose GPU. It is developing specialized ASICs optimized for transformer-based models and large-scale inference.

The logic is straightforward: GPU flexibility comes at a cost. A significant portion of hardware complexity exists to support a wide range of workloads. If infrastructure is mainly used for one class of models, a specialized chip may deliver better performance, lower energy consumption and a lower cost per token.

This is where Etched becomes strategically important.

It does not need to replace CUDA, dominate model training or become a universal computing platform. It only needs to prove that large, stable inference workloads can be served more economically without general-purpose GPUs.

If that model succeeds, the market may split into several layers:

* general-purpose GPUs for training and rapidly changing workloads; * specialized ASICs for high-volume inference; * custom hyperscaler chips for stable internal workloads.

Inference Is Becoming the Main Competitive Battlefield

Inference is the most vulnerable part of NVIDIA’s market.

Once a model has been trained, the priorities change. Cost, latency, throughput and energy efficiency become more important than maximum flexibility.

This creates room for Etched, Groq, Cerebras and custom cloud accelerators.

These platforms do not need to replace NVIDIA completely. They only need to capture workloads where specialization creates better economics.

The real risk for NVIDIA is therefore not one single competitor. It is the gradual fragmentation of the market across multiple specialized architectures.

Why NVIDIA Still Holds the Strongest Position

NVIDIA’s main defense remains its mature platform.

A cheaper chip can become more expensive in production if it requires code rewrites, team retraining, new monitoring systems and additional engineering support.

This is why NVIDIA is unlikely to lose leadership quickly.

But competitors do not need to replicate the entire NVIDIA ecosystem. They only need to win specific workloads where specialization matters more than flexibility.

Conclusion

NVIDIA will likely remain the leader in AI infrastructure, but the market is becoming more layered.

AMD and other vendors will compete in general-purpose accelerators. Hyperscalers will continue building custom chips. Etched and other ASIC companies will target high-volume inference. HBM, packaging and networking providers will gain greater strategic influence.

Etched matters because it is not offering a better GPU. It is challenging the idea that every major AI workload requires a general-purpose GPU at all.

The long-term threat to NVIDIA is not complete replacement. It is the possibility that a growing share of AI workloads will no longer need its most universal hardware.

This article is a strategic market-structure note. It is not investment advice.

Registered sources

No comments yet.